Your inventory can transform from an asset to a liability if not managed meticulously. We help you to automate the management of inventory, including details of lot and serial numbers, cost, quantity and dates, as the inventory moves through the process, without allowing scope for error. Inventory management software can also integrate with accounting and ERP systems

Inventory management is a collection of tools, techniques, and strategies for storing, tracking, delivering, and ordering inventory or stock. A large amount of capital, if not the majority of a company's capital is wrapped up in their inventory.

For that reason, it's incredibly important to control the coming and going of inventory as best you can to minimize losses and maximize profits – which is where inventory management techniques come into play.:

In order to run your business smoothly, you must have a well-functioning inventory management system. If you don't have one, it might cause a lot of trouble and start to disturb the execution of orders and day-to-day business.

Below is a list of some of the most popular and effective inventory management techniques you can use to improve your business.

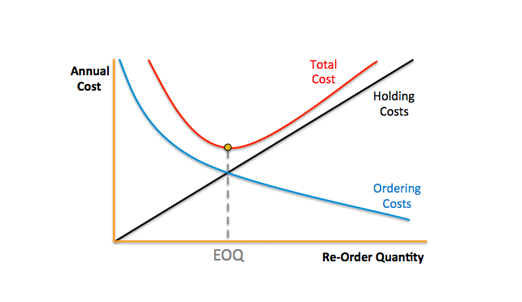

Economic order quantity is the lowest amount of inventory you must order to meet peak customer demand without going out of stock and without producing obsolete inventory. Its purpose is to reduce inventory as much as possible to keep the cost of inventory as low as possible.

To help you calculate EOQ, here is the formula from Kenneth Boyd, author of Cost Accounting for Dummies: Economic order quantity uses three variables: demand, relevant ordering cost, and relevant carrying cost. Use them to set up an EOQ formula:

Minimum order quantity (MOQ) is the lowest set amount of stock that a supplier is willing to sell. If you can't purchase the MOQ of a specific product, then the supplier won't sell it to you.

The purpose of minimum order quantities is to allow suppliers to increase their profits while getting rid of more inventory more quickly and weeding out the "bargain shoppers" simultaneously.

A minimum order quantity is set based on your total cost of inventory and any other expenses you have to pay before reaping any profit – which means MOQs help wholesalers stay profitable and maintain a healthy cash flow.

Volusion has a pretty nicely structured dashboard, with all of the main actions pointed out. If you're a new user just getting started with the platform, you will find a nice step-by-step wizard guiding you through the setup.

Just-in-Time Inventory Management is simply making what is needed, when it's needed, in the amount needed. Many companies operate on a "just-in-case" basis – holding a small amount of stock in case of an unexpected peak in demand.

JIT attempts to establish a "zero inventory" system by manufacturing goods to order; it operates on a "pull" system whereby an order comes through and initiates a cascade response throughout the entire supply chain – signaling to the staff they need to order inventory or begin producing the required item. Here are some of the benefits of just-in-time inventory:

Safety stock inventory is a small, surplus amount of inventory you keep on hand to guard against variability in market demand and lead times. Safety stock plays an integral role in the smooth operations of your supply chain in various ways.

Here are just a few:

FIFO (first in, first out) is an inventory accounting method that says the first items in your inventory are the first ones that leave – meaning you get rid of your oldest inventory first. LIFO (last in, first out) is an inventory accounting method that says the last items in your inventory are the first ones that leave – meaning you get rid of the newest inventory first.

If you handle food inventory management or operate any business with perishable items, then you pretty much have to use FIFO. Otherwise, you'll end up with obsolete inventory that you'll have to write-off as a loss. With that said, LIFO is a great method for non-perishable homogeneous goods like stone or brick. So, if you get a fresh batch of items like these, you don't need to rearrange your warehouse or rotate batches since they'll be the first ones out anyway.